You are sitting in a hospital in Paris. You have been admitted with a severe infection. The bill is going to be significant — possibly several lakhs. You are not panicking because you bought travel insurance before this trip. You have the documents. You have the policy number. You know you are covered.

Then three weeks after you return to Hyderabad, an email arrives.

Claim Denied.

This scenario is not rare. Most claim rejections happen due to exclusions or documentation errors, not because the claim itself was invalid. The insurance company is not necessarily being dishonest. The policy you bought did cover the situation you were in — but somewhere in the process, something was missed. A document was not submitted. A deadline was not met. A condition was not declared. A pre-approval was not obtained.

And the claim that should have protected you did not.

At BuildMyTrip, we have seen this happen to Indian travellers more times than we would like to count. This blog exists to make sure it never happens to you.

Why Travel Insurance Rejection Is a Growing Problem in India

Claim rejections are one of the key pain points that hold travellers back from getting travel insurance in India and contribute to low adoption across the country. The irony is that the people who skip travel insurance often do so because they have heard too many stories of claims being rejected. And some of those stories are completely valid.

In 2026, as global travel hits record highs, insurance companies have become more technologically advanced, using AI to scrutinise claims with surgical precision. While this means faster payouts for some, it also means a single missing receipt or a minor omission can lead to automatic rejection.

Understanding exactly how claims get rejected — and what to do about each one — is the only way to make sure your insurance actually works when you need it.

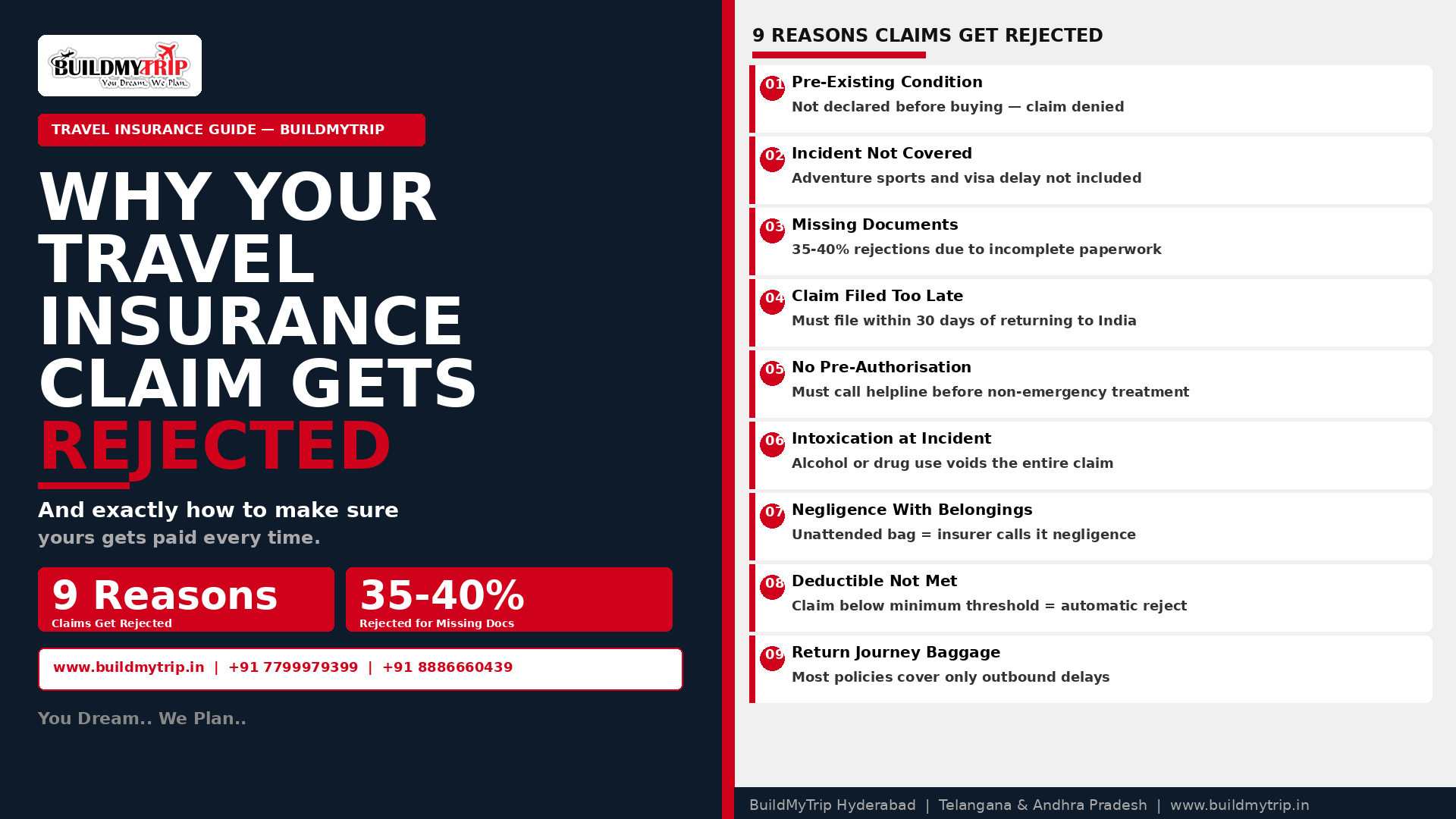

Rejection Reason 1 — Pre-Existing Medical Conditions

This is the single most common reason Indian travellers have their medical claims rejected abroad.

Pre-existing disease exclusion means that if you had diabetes, heart trouble, asthma, or recent treatment before the trip, related overseas treatment may be denied unless the policy allows it. This is one of the top claim rejection reasons because travellers often assume stable means covered.

The insurance company's position is this — if you had a condition before you bought the policy, any medical event related to that condition is not their responsibility unless you specifically declared it and paid for the appropriate cover.

What this means in practice is that a diabetic traveller who has a diabetes-related complication in Europe will likely have their claim rejected if they did not disclose their diabetes when buying the policy. A person with a heart condition who experiences cardiac symptoms abroad will face the same outcome.

The fix is simple but requires honesty. Declare every current illness, medicine, and past surgery before you pay for the policy. Some insurers will offer coverage for pre-existing conditions with a higher premium or a waiting period. Others will exclude it entirely but at least you will know in advance. What you cannot do is fail to declare it and then expect the claim to be paid.

Rejection Reason 2 — The Incident Was Not Actually Covered

A very common reason for claim rejection is when the incident is not covered under the policy but the traveller assumes that it is. For example, one might think that adventure sports are covered in their travel policy but it is not necessary that they are. Moreover some policies cover visa delays and some do not.

This is the gap between what people think travel insurance covers and what it actually covers. Most standard travel insurance policies do not automatically include adventure sports like skiing, scuba diving, trekking above certain altitudes, parasailing or white water rafting. If you participate in any of these without buying the specific add-on cover, any resulting injury will not be covered.

Trip cancellation is another area of significant misunderstanding. Many times, insured travellers make the assumption that trip cancellation coverage ensures they can file a claim if their trip gets cancelled for any reason. This is however not the case. The reasons for trip cancellation are clearly stated in the policy terms and conditions — hospitalisation, sickness, injury, death to an immediate family member — and if neither of these situations occur, the insured cannot file a trip cancellation claim and expect to be compensated.

Changing your mind about the trip, work getting busy, or deciding you do not feel like travelling are not covered reasons. Neither is a visa rejection in most cases, unless you specifically bought a policy that includes visa rejection coverage.

The fix is to read the policy document before you buy it — not after you return. Focus specifically on the exclusions section. Read the exclusions before you pay, not after you travel.

Rejection Reason 3 — Missing or Incomplete Documentation

Roughly 35 to 40 percent of all claim rejections in 2026 are due to insufficient evidence. This is entirely avoidable and yet it remains one of the leading causes of rejection.

Every type of claim requires specific documentation. Medical claims require hospital bills, doctor certificates, prescription records, diagnostic reports and discharge summaries. Flight delay claims require an official delay certificate from the airline — not just a screenshot of the departure board or a WhatsApp message. Baggage loss claims require a Property Irregularity Report filed with the airline at the airport. Trip cancellation claims require the specific documentation supporting your reason — a medical certificate, death certificate, or employer letter depending on the reason.

You claim a 12-hour flight delay but you do not provide an official delay report from the airline. This is a heartbreaking reason for rejection in travel insurance.

The fix is to collect every document in real time as the incident happens. If your flight is delayed, go to the airline desk and ask for an official delay certificate before you leave the airport. If you are hospitalised, collect every bill, prescription, report and discharge summary before you check out. If your baggage is lost, file the PIR report at the airport immediately — do not wait until you reach the hotel.

Keep physical copies and photograph everything on your phone the moment you receive it.

Rejection Reason 4 — Claim Filed Too Late

Every travel insurance policy has a specific time limit within which you must file your claim after returning to India. This is typically 30 days from the date of the incident or 30 days after returning home, depending on the insurer and the type of claim.

Certain policies permit claims after returning within a designated period — for instance 30 days. However all invoices and documents must be submitted within this period.

Indian travellers frequently make the mistake of filing their claim weeks after returning, assuming that the insurance company will be understanding about delays. They are not. The deadline is a contractual obligation and missing it gives the insurer a valid technical reason to reject the claim regardless of its merit.

The fix is to file your claim as soon as you return to India — ideally within the first week. Do not wait until you are fully settled back into your routine. The documentation is freshest immediately after the incident and the deadline clock is running from the moment the event occurred.

Rejection Reason 5 — No Pre-Authorisation for Medical Treatment

This is one of the least understood rejection reasons and it catches many Indian travellers completely off guard.

Another common reason for rejection of a claim is the lack of approval from the insurance company prior to seeking medical treatment, or seeking reimbursement for a medical expense not incurred under the policy.

Most travel insurance policies require you to call the insurer's 24-hour helpline before seeking non-emergency medical treatment abroad. The insurer then either arranges cashless treatment at a network hospital or gives you pre-authorisation for reimbursement. If you go directly to a hospital without calling the helpline first — even if the treatment is legitimate and covered — the insurer may reject the claim on the grounds that no pre-authorisation was obtained.

Emergency situations are typically handled differently and require you to seek treatment first and notify the insurer within a specified period — usually 24 to 48 hours after the emergency.

The fix is to save your insurer's 24-hour international helpline number in your phone before you travel. The moment a non-emergency medical situation arises, call them first. For emergencies, seek treatment immediately and call them at the earliest opportunity.

Rejection Reason 6 — Intoxication at the Time of the Incident

If an accident happens after heavy drinking, drug use, or deliberate self-harm, insurers usually refuse payment. Disputes often begin when the hospital record mentions alcohol.

The policy language in most Indian travel insurance contracts specifically excludes any claim where the insured was under the influence of alcohol or controlled substances at the time of the incident. This applies to accidents, medical emergencies, and loss of belongings. If you fall and injure yourself after drinking at a restaurant in Europe and the hospital record notes alcohol consumption, the insurer has grounds to reject the claim.

This is a straightforward exclusion to understand. Exercise appropriate judgment when travelling.

Rejection Reason 7 — Negligence With Your Belongings

Insurers expect you to take reasonable care of your property. You leave your laptop bag on a café chair to grab a napkin. When you turn back it is gone. The insurer labels this as negligence because the item was unattended in a public place.

Baggage and personal belongings claims are frequently rejected on the grounds of negligence. Leaving your bag unattended in a public space, leaving valuables in a hotel room without using the safe, leaving electronics in a checked bag that gets lost — these are all situations where the insurer may argue that you failed to take reasonable care of your property.

If it is not in your hand or a locked safe it is considered unattended. Never leave bags in the custody of a common carrier like an airline if they contain high-value electronics or jewellery — keep those in your carry-on.

The fix is to treat your belongings abroad with the same vigilance you would apply in any crowded public place. Keep valuables on your person or in the hotel safe. Never leave bags unattended in cafes, on trains, or at tourist sites.

Rejection Reason 8 — The Deductible Was Not Met

In some policies travellers have to pay a part of the expense before the insurance pays. For example if your baggage delay is covered under your policy but the coverage starts after 5 hours, your claim will be rejected if the delay happens only for four hours. Another example would be if medical bills are covered under your policy but only if you pay over Rs.5,000, your claim would be rejected if the total bill is Rs.4,000.

Deductibles and waiting periods exist in almost every travel insurance policy. Understanding them before you travel means you know exactly when you are entitled to claim and when you are not. Many Indian travellers try to claim amounts below the deductible threshold and are confused when the claim is rejected.

Rejection Reason 9 — Baggage Delay on Return Journey

This is a particularly specific exclusion that surprises many travellers.

Most travellers assume that since baggage delay is a cover under the policy they can file a claim if there is a baggage delay on either their onward or return journeys. But many travel insurance policies do not cover baggage delay on the return journey when the insured is returning to India, and hence such a claim will be rejected.

Baggage delay cover typically applies only to the outbound journey — when your luggage is delayed at your destination. If your bag is delayed on the way back to Hyderabad, most standard policies will not cover the expenses because you are returning to your home country where you presumably have access to your wardrobe and essentials.

Check specifically whether your policy covers both directions before you buy.

What to Do If Your Claim Is Rejected

If your travel insurance claim is rejected despite your best efforts, read the rejection letter carefully — it usually mentions the exact reason. Collect any missing information. If it is a document issue fix it and ask for reconsideration.

Sometimes rejections are based on missing documents that you can still provide. Submit a formal appeal within 30 days addressing each rejection reason point by point. Include additional documentation if available.

If the appeal is also rejected and you believe the rejection is unjustified, you can file a complaint with the Insurance Regulatory and Development Authority of India. IRDAI has a grievance redressal process and insurance companies are required to respond to IRDAI complaints within specific timelines.

The BuildMyTrip Approach to Travel Insurance

When you book a trip with us, we do not treat travel insurance as a checkbox — something to buy because it is required for the visa. We help you understand what the policy covers, what it excludes, what the claim process looks like, and what documentation to collect if something goes wrong.

We recommend policies that have clear claim processes, responsive 24-hour helplines and fair track records on settlement. We also tell our customers to save the insurer's helpline number in their phone before departure and to call it immediately in any non-emergency medical situation.

Travel insurance that pays when you need it is not about luck. It is about buying the right policy, understanding it properly, and following the right steps when something goes wrong. That is something we help every BuildMyTrip customer do as part of planning their trip.

Call us today for a free consultation on your next international trip.

📞 +91 7799979399 📞 +91 8886660439 🌐 www.buildmytrip.in 📍 Hyderabad, Telangana

You Dream.. We Plan..

Frequently Asked Questions

What is the most common reason travel insurance claims are rejected in India?

The most common reasons include non-disclosure of medical history, incomplete documents, missing claim timelines and exclusions mentioned in the policy wording. Pre-existing medical conditions that were not declared at the time of buying the policy are consistently the leading cause of rejected medical claims.

How soon after returning to India should I file a travel insurance claim?

File within the first week of returning — ideally within three to five days. Most policies have a 30-day deadline from the date of the incident or return date but the sooner you file the fresher your documentation is and the less likely you are to miss any required paperwork.

Does travel insurance cover trip cancellation for any reason?

No. Trip cancellation coverage only pays out for specific covered reasons listed in the policy — typically hospitalisation of the traveller or an immediate family member, death of an immediate family member, or natural disasters at the destination. Cancelling because of work commitments or change of plans is not covered.

Is adventure sports covered under standard travel insurance?

Skiing, scuba diving, trekking above a certain altitude or parasailing may be excluded unless you bought the add-on. Always check the policy specifically for adventure sports exclusions and buy the appropriate add-on before participating in any adventure activity abroad.

What should I do immediately if my baggage is lost at a foreign airport?

File a Property Irregularity Report with the airline at the airport before leaving the baggage claim area. Get a copy of the PIR with a reference number. Keep all receipts for essential items you purchase due to the delay. Contact your insurer's helpline as soon as possible. These steps are non-negotiable for a successful baggage loss or delay claim.

How much travel insurance coverage is recommended for a Europe trip?

For international travel a minimum medical cover of USD 100,000 to USD 250,000 is advisable. Higher coverage is recommended for countries like the US and Europe. Schengen visa requirements specify a minimum of EUR 30,000 in medical coverage but a higher limit significantly protects you in the event of serious illness or injury.